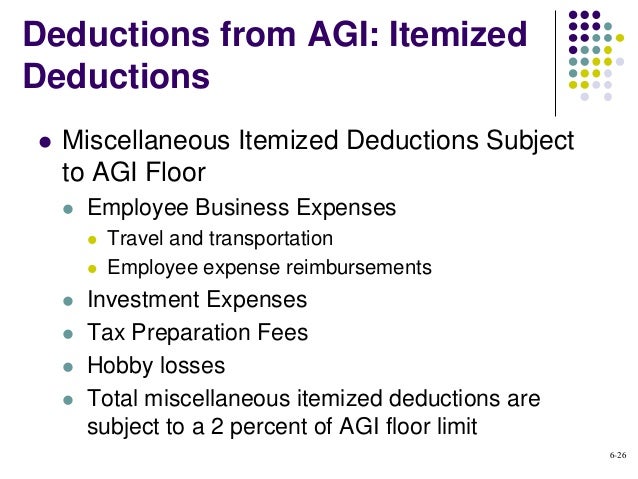

2 Floor Limitation Miscellaneous Deductions

Acct321 Chapter 06

What Your Itemized Deductions On Schedule A Will Look Like After Tax Reform Piearcy Financial Solutions Llc

Does The Standard Deduction Or Itemizing Make Sense For Your Taxes

Tax Deductions For Individuals A Summary Everycrsreport Com

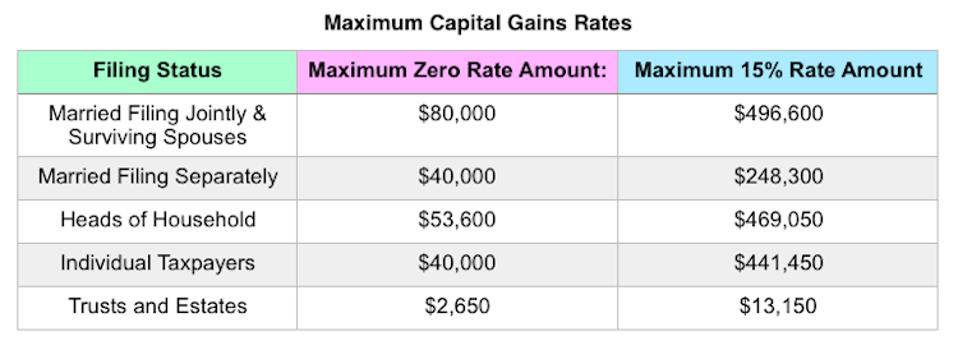

Key Retirement And Tax Numbers For 2018 Alexandria Capital

What Itemized Deductions Will Look Like In 2018 680 The Fan Wcnn Am

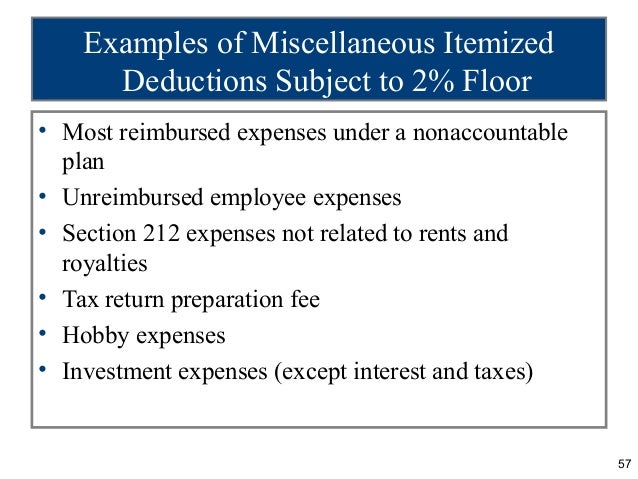

Miscellaneous itemized deductions are those deductions that would have been subject to the 2 of adjusted gross income limitation.

2 floor limitation miscellaneous deductions. The 2 rule referred to the limitation on certain miscellaneous itemized deductions which included things like unreimbursed job expenses tax prep investment advisory fees and safe deposit box rentals. The regulations will apply to tax years beginning on or after may 9 2014. This publication covers the following topics. Miscellaneous deductions are deductions that do not fit into other categories of the tax code.

Starting on january 1 2018 and running through december 31 2026 individuals will no longer have the ability to deduct the excess expenses listed below as itemized deductions on their 1040s. 2 percent floor on miscellaneous itemized deductions. There are two types of miscellaneous deductions. Deductible expenses subject to the 2 floor includes.

2 percent floor on miscellaneous itemized deductions. Expenses for uniforms and special clothing. Except as otherwise provided in paragraph d of this section to the extent that any limitation or restriction is placed on the amount of a miscellaneous itemized deduction that limitation shall apply prior to the application of the 2 percent floor. Miscellaneous itemized deductions subject to the 2 floor aren t deductible for tax years 2018 through 2025.

As of the 2018 tax year itemized deductions for job related expenses or other miscellaneous expenses outlined below that exceeded 2 of your income have been suspended. These losses are not subject to the 2 limit on miscellaneous itemized deductions. Unreimbursed employee business expenses such as. The irs issued final regulations on the controversial question of which costs incurred by trusts and estates are subject to the 2 floor on miscellaneous deductions under sec.

For example in the case of an expense for food or beverages only 80 percent of which is allowable as a deduction. This section shall be applied before the application of the dollar limitation of the second sentence of section 162 a relating to trade or business expenses. 1 deductions subject to the 2 limit these deductions allow you to deduct only the amount of expense that is over 2 of your adjusted gross income or agi. However deductions under section 67 e 1 continue to be deductible if they are costs that are incurred in connection with the administration of an estate or a non grantor trust that would not have been incurred if the property were.

However the deduction is limited to the amount of taxable. For tax years previous to 2018 if you itemize your deductions part of the expenses that you claim as deductions may be limited by the 2 rule deductions that are included are unreimbursed employee expenses expenses. Investment interest remains deductible for taxpayers who itemize.

Planning For The Parallel Universe Of The Net Investment Income Tax

2106 Employee Business Expenses 2106 Schedule1

Https Lawpracticecle Com Wp Content Uploads 2019 01 Lawpracticecle The New Tax Cuts And Jobs Act Pdf

Taxation Of Individuals And Business Entities 2018 Edition 9th Editio

Contractors And Tax Reform Key Aspects To Know Explore Our Thinking Plante Moran

New Tax Changes For 2018 Tax Cuts And Jobs Act Mycpa Net

Where Have All The Deductions Gone Key Private Bank

2013 Cch Basic Principles Ch06

Irs Releases 2020 Tax Rate Tables Standard Deduction Amounts And More Tncpa

Ppt Ch 09

Https Www Drakesoftware Com Sharedassets Manuals 2016 Fiduciaries Pdf

Https Www Drakesoftware Com Sharedassets Manuals 2018 Fiduciaries Pdf

Https Www Drakesoftware Com Sharedassets Manuals 2012 2012 20drake 20software 20manual 20supplement 20fiduciaries 20 1041 Pdf

How Did The Tcja Change The Standard Deduction And Itemized Deductions Tax Policy Center

2019 2020 Tax Return Itemized Tax Deductions On Schedule A

The Tax Cut Impacts Investors In Negative And Positive Ways Greentradertax

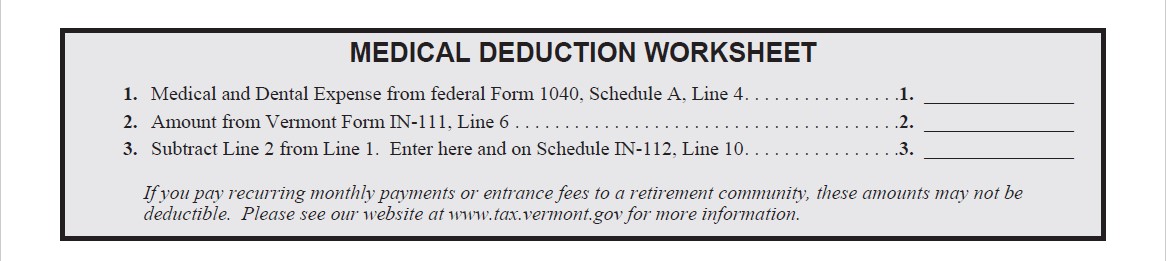

Vermont Medical Deduction Department Of Taxes

Iowa Provides Itemized Deduction Guidance Tax Accounting Blog

Https Www Actec Org Assets 1 6 Actec Comments On 2018 61 Pdf

3 Itemized Deduction Changes With Tax Reform H R Block

Individual Tax Changes Itemized Deduction Virginia Cpa

How To Deduct Borrowing Fees When Selling Stocks Short

Miscellaneous Tax Deductions To Claim On Your Tax Return

Gale Academic Onefile Document High Income Tax Returns For 2013

Https Www Mncpa Org Mncpa Media Documents Shared Legislative Legislative Tax Guide Pdf

/taxes-5bfc47be46e0fb0026623559.jpg)

An Overview Of Itemized Deductions

Tax Guide Cpa For Real Estate Investors Real Estate Tax Accountant

Gale Academic Onefile Document Individual Income Tax Returns 1999

Itemized Deductions In 2018 5 Things To Know Credit Karma Tax

Https Www Aicpa Org Content Dam Aicpa Advocacy Tax Downloadabledocuments 20181031 Comment Letter On Notice 2018 61 Pdf

What Is The Standard Deduction Vs Itemized Deduction H R Block

Home Office Expenses Of A Small Business Organized As A Corporation Steven M Vogt Cpa Ea

The Tcja Impact On Estate And Trust Miscellaneous Deductions Sc H Group

Treatment Of Legal Fees Incurred By Individuals

Limits On Itemized Deductions How Itemized Deductions Work Howstuffworks

Proposed Regulations Upon Which Taxpayers May Rely Issued For Excess Deductions On Termination Current Federal Tax Developments

Itemized Deduction Archives Montana Department Of Revenue

Pastors Can No Longer Itemize Deductions For Busine Church Law Tax

Changes To The Employee Business Expense Deduction Block Advisors Block Advisors

A List Of Eliminated Tax Deductions For 2018 Returns Taxact Blog

Income Taxes Taxanswers

Employee Paid Business Expenses The Cpa Journal

Klr The New Tax Law And Its Impact On Itemized Deductions

/GettyImages-185121670-3e5dcbc98b0a4409914ea75fbe557091.jpg)